Does the Stock Market Feel the Holiday Spirit?

Month-to-month stock swings are impossible to predict—except for the one that happens after the holiday season. Meet the January Effect.

It’s a truism, best expressed by author Mark Twain, that the stock market doesn’t distinguish between months. As Twain humorously noted in his novel Pudd’nhead Wilson: “October. This is one of the peculiarly dangerous months to speculate in stocks. The others are July, January, September, April, November, May, March, June, December, August, and February.”

There is one exception to that rule, an interesting anomaly known as the January Effect or the Turn of the Year effect (documented separately by finance professors Donald B. Keim and Marc Reinganum in 1983). This phenomenon sees stock prices, particularly those of small-cap stocks, rising more in January than in other months. The January Effect sometimes overlaps with the Santa Claus Rally, which is the rise in stock prices during December and January.

Researchers and practitioners have proposed several explanations for these anomalies, which are more about rational investor behavior than holiday magic. Here are some common theories:

- Tax-loss harvesting: Investors sell poorly performing stocks in December to realize tax losses that can offset gains elsewhere in their portfolios. The selling depresses stock prices, which then recover in January as the selling pressure eases, thus creating an uptick in prices.

- Year-end bonuses: Some investors use their year-end bonuses to buy stocks in early January, driving up prices.

- Portfolio rebalancing: Investors and institutions often rebalance their portfolios at the start of the year, leading to increased buying activity.

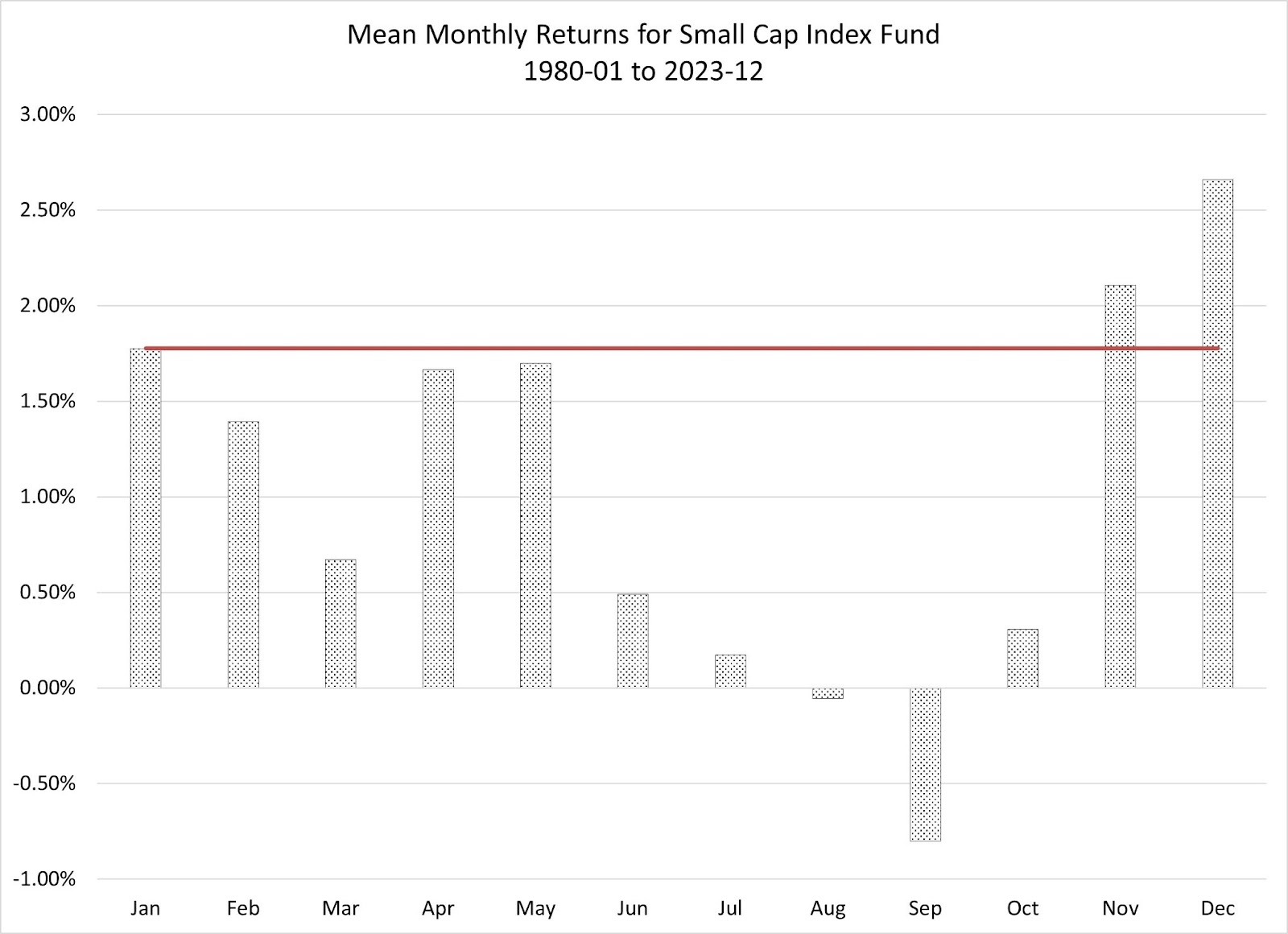

The January Effect is more pronounced in small-cap stocks because they are less liquid than larger stocks. Less liquidity means that increased buying and selling activity can more easily move their prices. Between 1980 and 2023, the average January return for the Vanguard Small Cap Index Fund (NAESX) was higher than the returns in nine of the other 11 months.

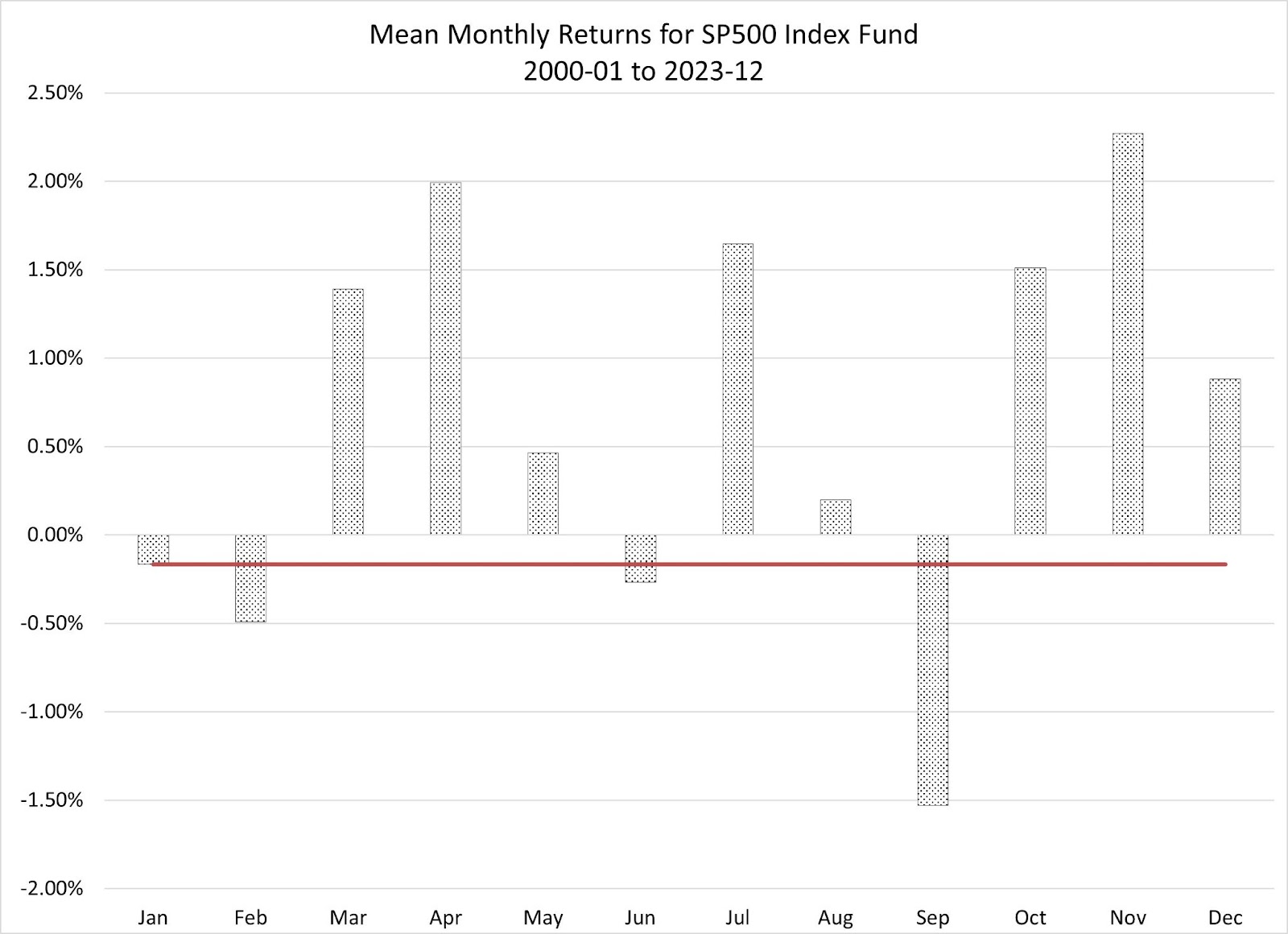

However, as we would predict, the pattern is less evident in large, very liquid stocks. For example, the average January return for the Vanguard SP500 Index fund (VFINX), which contains large stocks, is the fifth-lowest of the year.

The existence of any predictable stock market anomaly, like the January effect, runs up against the finance theory of efficient markets that states that it should be impossible to reliably predict that the stock market will perform better in one month than in any other. This is because smart traders would anticipate the January Effect and buy stocks in December, and end up nullifying the effect.

So what has happened to the January effect since it was discovered?

The data shows that the effect has indeed weakened in recent years. The publishing of the research that documents the anomaly had the effect of alerting investors to this potential money making opportunity.

The weakening of the effect is also likely due to several changes in the stock market that resulted in anomalies going away. In 2001, Decimalization (stock prices being quoted in $0.01 increments rather than the $0.125 amounts) reduced the cost of trading. And, more recently, the emergence of algorithmic (computer driven) and high-frequency trading accelerated the speed of trading. These changes, coupled with the rise of multibillion-dollar hedge funds, created a pool of large investors able to exploit pricing inefficiencies quickly.

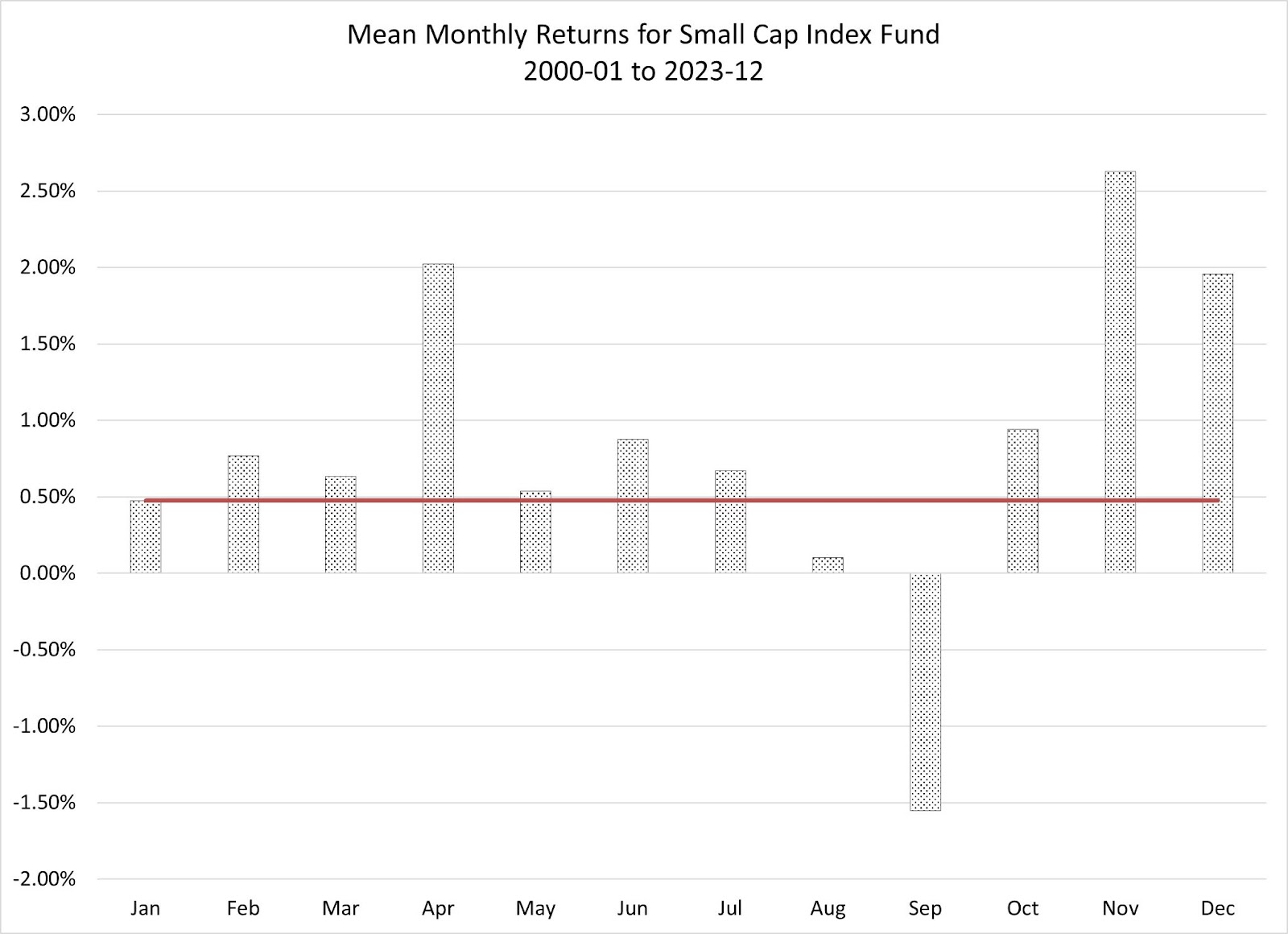

As a result, it appears that today, pricing anomalies such as the January Effect have largely been arbitraged away. During the 1980s and 1990s, the January return topped 2.5% for both the SP500 and the Small Cap index funds, larger than the return in any of the other 11 months. But, the effect is small or non-existent during the 2000-2023 period. In fact, the mean January return for the SP500 Index fund was actually negative during 2000-2023!

Will the January Effect occur this year? Borrowing from Mark Twain, January is as likely to outperform the other months as any other of the 11 months. But joking aside, as finance researchers, we would recommend that investors exercise caution. Prior research has shown that it’s generally wise for investors to focus on steadily investing in a broadly diversified, low-cost portfolio over a long period, rather than chasing short-term anomalies. Or, as finance professors Brad Barber and Terrance Odean once showed, “trading is hazardous to your wealth!” Even the Oracle of Omaha (Warren Buffett) would agree with that view.

Srini Krisnamurthy is an associate professor of finance. His research focuses on corporate finance, mergers and acquisitions, asset management and capital markets.

Richard Warr is associate dean for faculty and research. His research focuses on information transmission in markets, equity valuation, short selling, capital structure, risk management and market microstructure.

This post was originally published in Poole Thought Leadership.

- Categories: